Flowcharts: Should I Pay Off My Mortgage or My Debt(s)?

Debt complicates not only our finances, but our emotions too. Much of the stress surrounding debt simply comes from not addressing it in the first place.

Maybe it's time to consider some of your options.

We're here to have a more productive conversation around debt, develop strong reasons for paying off your debt, and identify the most optimal path for getting there.

Should I Pay Off My Mortgage?

Many say purchasing a home is one of the biggest decisions you make in your life, but very few talk about how big of a decision it is to pay off your home.

There’s a lot of disagreement on this topic, and some of our clients often find themselves lost and uncertain as to what they should do. We're here to help you gain a more nuanced understanding of why and maybe why not to consider paying off your mortgage.

This flowchart covers important decision-making factors to consider when paying off your mortgage, such as:

Thoroughly weighing the pros and cons involved in this big decision, and how they may specifically relate to your financial situation.

Recognizing what degree of flexibility you may or may not have after paying off the mortgage.

Considering any tax implications that may result from paying off the mortgage.

Identifying sound reasons for paying off the mortgage, and determining the best course of action, if applicable.

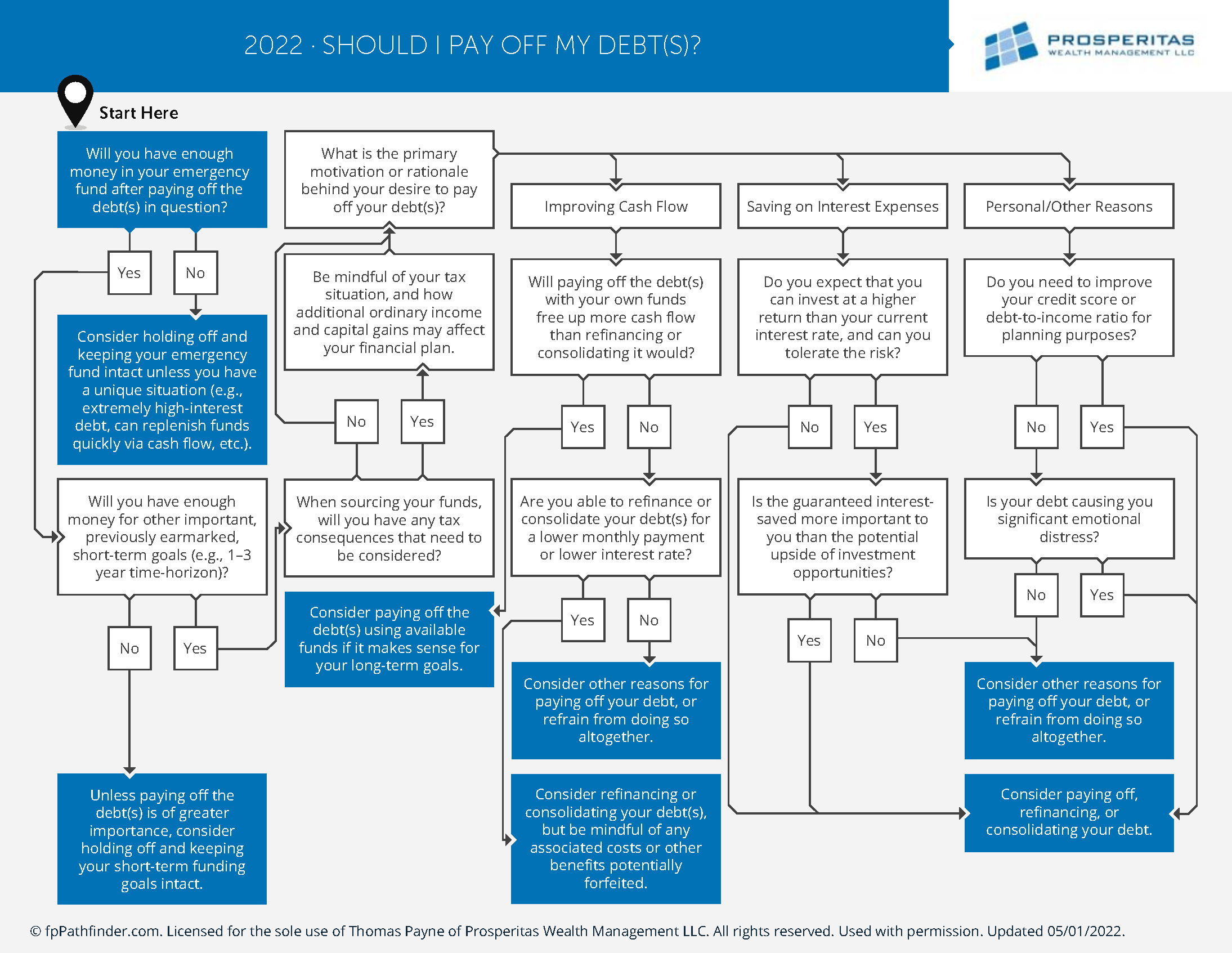

Should I Pay Off My Debt(s)

This flowchart covers important decision-making factors to consider when tackling any other non-mortgage debt(s), such as:

Maintaining an emergency fund, despite any potential conflicting priorities.

Balancing the importance of paying off debt without jeopardizing any other financial goals you may have previously set for yourself.

Identifying sound rationale and motivations for paying off debt, and determining the best course of action.

Should you have any questions, please don't hesitate to contact us.